US housing market statistics for 2026 show a market defined by slow price growth, constrained sales volume, and a persistent affordability gap. Existing-home sales reached 4.02 million (SAAR) in April 2026 with a median price of $417,700, according to NAR. That marks the 34th consecutive month of year-over-year price increases, but the pace of appreciation has decelerated sharply to under 1%.

This page tracks the core metrics that define the US housing market: sales volume, median prices, inventory levels, mortgage rates, new construction, builder sentiment, and regional breakdowns. All data is sourced from NAR, Redfin, Freddie Mac, the US Census Bureau, and Zillow Research. Updated quarterly.

To put 2026’s numbers in historical context: the pre-pandemic norm for existing-home sales was 5.34 million in 2019. The current pace of 4.02 million represents a 25% deficit from that baseline, now sustained for three consecutive years. The combination of elevated mortgage rates, record-high prices, and the lock-in effect has created a structural gridlock in the resale market that gradual improvements in inventory have not yet resolved.

| Metric | Latest Value | Period | YoY Change |

|---|---|---|---|

| Existing-Home Sales (SAAR) | 4.02 million | April 2026 | Flat |

| Median Existing-Home Price | $417,700 | April 2026 | +0.9% |

| 30-Year Fixed Mortgage Rate | 6.51% | Week of May 21, 2026 | -0.35 pts |

| Housing Inventory | 1.47 million units | April 2026 | +5.8% |

| Months of Supply | 4.4 months | April 2026 | +0.1 mo |

| New Home Sales (SAAR) | 682,000 | March 2026 | +3.3% |

| Median New Home Price | $387,400 | March 2026 | -6.2% |

| Housing Starts (SAAR) | 1.465 million | April 2026 | -2.1% |

| Building Permits (SAAR) | 1.442 million | April 2026 | -0.2% |

| NAHB Builder Confidence (HMI) | 37 | May 2026 | -20 pts vs May 2024 |

| Median Days on Market | 32 days | April 2026 | +3 days |

| First-Time Buyer Share | 33% | April 2026 | -1 pt |

| Housing Affordability Index | 110.6 | April 2026 | +9.2 pts |

Sources: NAR Existing-Home Sales, April 2026; Freddie Mac PMMS, May 21, 2026; US Census Bureau, March-April 2026; NAHB/Wells Fargo HMI, May 2026

The summary table reflects a market stuck in a narrow band. Sales volume has hovered near 4 million annualized for three consecutive years with no breakaway surge. Price growth has decelerated from 6% year-over-year in late 2025 to under 1% by spring 2026. Inventory is improving but remains below the 5-to-6 month supply range that NAR considers a balanced market.

Existing-Home Sales and Median Price

| Month | Sales (SAAR, millions) | Median Price | MoM Change (Sales) | YoY Change (Price) |

|---|---|---|---|---|

| April 2026 | 4.02 | $417,700 | +0.2% | +0.9% |

| March 2026 | 3.98 | $398,000 | -3.6% | +0.3% |

| February 2026 | 4.09 | $398,000 | +1.7% | +0.3% |

| January 2026 | 4.02 | $396,900 | -2.3% | +4.5% |

| December 2025 | 4.16 | $404,400 | +1.5% | +6.0% |

| November 2025 | 4.10 | $406,100 | +3.8% | +4.2% |

| October 2025 | 3.95 | $407,200 | +3.4% | +4.0% |

| April 2025 | 4.00 | $414,000 | -0.5% | +1.8% |

| April 2024 | 4.08 | $406,600 | N/A | +5.7% |

| April 2019 (pre-pandemic) | 5.19 | $267,300 | N/A | N/A |

Source: NAR Existing-Home Sales Reports, 2019-2026

Sales volume has remained locked between 3.95 and 4.16 million SAAR since October 2025, a range so narrow it represents functional stagnation. The April 2026 pace of 4.02 million is virtually identical to April 2025’s 4.00 million and remains 25% below the pre-pandemic April 2019 rate of 5.19 million. This three-year suppression of sales volume is without precedent in modern housing data outside of the 2008-2011 crisis.

The April 2026 median price of $417,700 represents the highest April on record, though year-over-year appreciation has compressed sharply. Price growth decelerated from 6.0% in December 2025 to just 0.9% by April 2026. NAR Chief Economist Lawrence Yun attributed the slowdown to “lower consumer confidence and softer job growth” combined with gradually improving supply.

The S&P CoreLogic Case-Shiller US National Home Price Index reinforces the deceleration trend. It recorded just 0.91% year-over-year growth in January 2026 on a seasonally adjusted basis. When adjusted for inflation, this translates to a 1.44% decline in real terms, meaning the typical American home lost purchasing-power value even as its nominal price inched higher.

A useful way to understand the price trajectory is the gap between new and existing home prices. Existing homes carried a median of $417,700 in April 2026, while new homes sold at a median of $387,400 in March 2026, a $30,300 discount.

This inversion, where new construction costs less than existing stock, reflects aggressive builder price cuts and concessions to move inventory. Historically, new homes carry a premium over existing homes, making the current inversion a notable data anomaly.

For monthly breakdowns, see Median Home Price in the US and Home Sales Statistics.

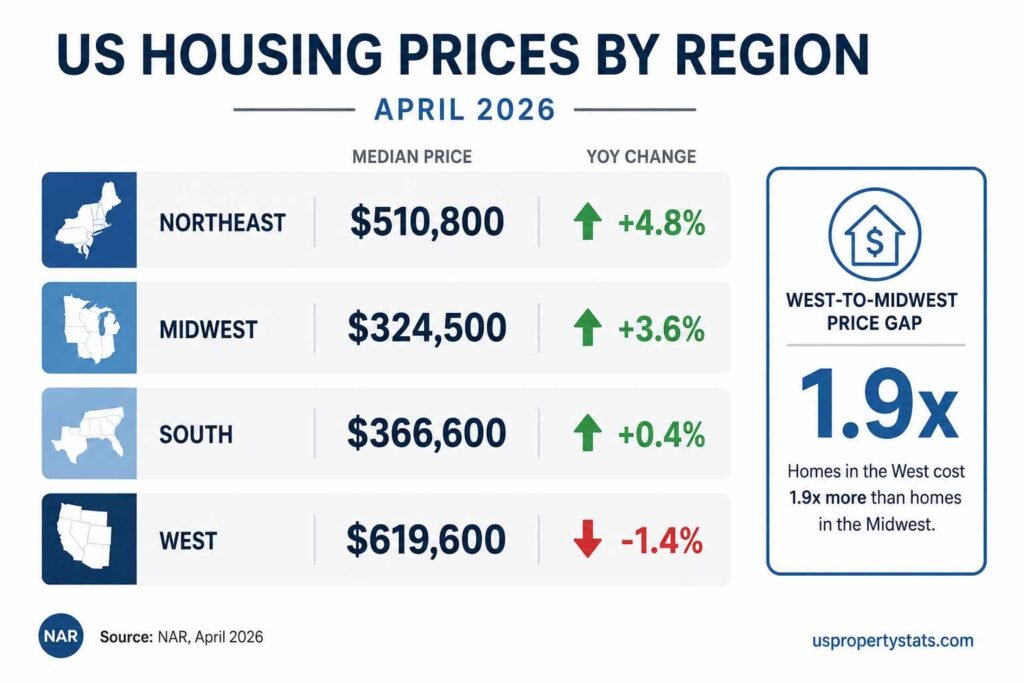

Regional Price Breakdown

| Region | Median Price (April 2026) | YoY Change | Sales (SAAR, thousands) | MoM Sales Change |

|---|---|---|---|---|

| Northeast | $510,800 | +4.8% | 500 | Flat |

| Midwest | $324,500 | +3.6% | 950 | +2.2% |

| South | $366,600 | +0.4% | 1,790 | +0.6% |

| West | $619,600 | -1.4% | 750 | -2.6% |

Source: NAR Existing-Home Sales Report, April 2026

The regional data reveals a two-speed market. The Northeast and Midwest are posting above-average price growth driven by relative affordability and constrained supply. States like New Jersey (+5.6%), Connecticut (+5.3%), and Illinois (+4.9%) are outpacing the national average by wide margins, drawing buyers priced out of coastal markets.

The West is the only region with negative year-over-year price growth. This correction is concentrated in markets that saw the sharpest pandemic-era run-ups: Colorado (-1.3%), parts of Arizona, and several Florida metros (-2.4%).

Post-pandemic supply is catching up with demand in these Sun Belt markets, and rising insurance costs in Florida are creating an additional headwind that other regions do not face.

The South accounts for the largest volume share at 1.79 million annualized sales but is showing near-flat price appreciation (+0.4%), consistent with higher inventory levels across Texas, Florida, and Georgia. For state-by-state analysis, see Average Home Price by State and Home Appreciation Rates by State.

What the Regional Split Means for National Statistics?

National median price figures can obscure significant local variation. The $295,300 gap between the West ($619,600) and Midwest ($324,500) represents a 1.9x multiple. An identical home costs nearly twice as much depending on geography.

Buyers in the Midwest need roughly $65,000 in household income to qualify for a median-priced home at current rates. In the West, that threshold exceeds $125,000.

This divergence has accelerated since 2020. Before the pandemic, the West-to-Midwest price ratio was approximately 1.7x. The widening reflects both disproportionate price growth in the West during 2020-2022 and the Midwest’s later entry into the appreciation cycle.

Inventory, Supply, and the Lock-In Effect

| Month | Active Inventory | Months of Supply | YoY Inventory Change |

|---|---|---|---|

| April 2026 | 1,470,000 | 4.4 | +5.8% |

| March 2026 | 1,360,000 | 4.1 | +9.0% |

| February 2026 | 1,290,000 | 3.8 | +8.8% |

| January 2026 | 1,180,000 | 3.5 | +7.5% |

| April 2025 | 1,390,000 | 4.3 | +20.8% |

| April 2024 | 1,210,000 | 3.5 | N/A |

| Pre-pandemic avg (2017-2019) | ~1,850,000 | ~4.3 | N/A |

Source: NAR Existing-Home Sales, January 2024 through April 2026

Inventory rose to 1.47 million units in April 2026, a 5.8% increase from one year ago and the highest April reading since 2020. Months of supply climbed to 4.4, approaching the lower bound of the 5-to-6 month range that NAR defines as a balanced market.

The improvement is real but incremental: current inventory remains approximately 20% below the pre-pandemic average of roughly 1.85 million units.

NAR’s Yun has stated that “an additional 300,000 to 500,000 homes for sale would help bring the market closer to normal conditions and allow consumers to make purchase decisions without feeling rushed.” At the current trajectory of ~5-6% annual inventory growth, reaching that threshold is a 2027-2028 event.

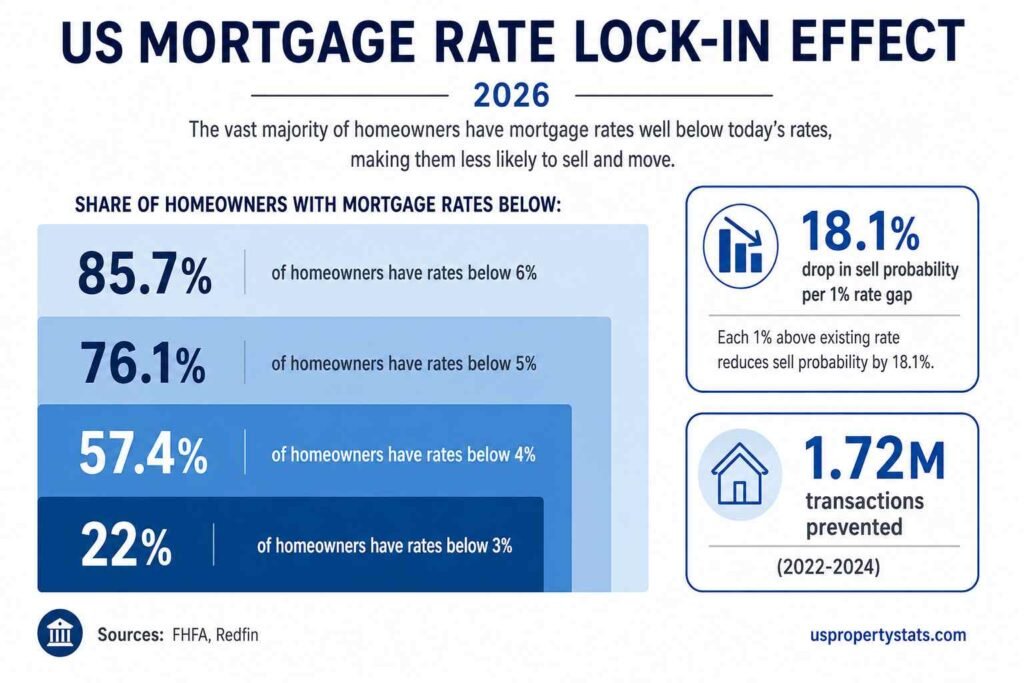

The Lock-In Effect

The primary constraint on inventory is the mortgage lock-in effect. According to FHFA research, each percentage point that current market rates exceed a homeowner’s existing fixed rate reduces their probability of selling by 18.1%.

With the 30-year fixed rate at 6.51% and an estimated 52% of mortgage holders carrying rates below 4%, the financial penalty for selling remains severe for the majority of homeowners.

A Redfin analysis of FHFA National Mortgage Database data shows the breakdown: 85.7% of mortgaged homeowners have rates below 6%, 76.1% below 5%, 57.4% below 4%, and 22% below 3%. The lock-in effect prevented an estimated 1.72 million transactions between Q2 2022 and Q2 2024 alone, according to FHFA, and increased national home prices by an estimated 7%.

The thaw is happening, but slowly. The share of sub-3% mortgages edged down to 19.7% in Q4 2025, from a peak of 24.6% in Q1 2022. Life events (divorces, job relocations, deaths, family growth) are gradually forcing sales regardless of rate differentials, but the pace is measured in years, not quarters.

Redfin tracks 1.93 million homes for sale nationally as of March 2026, with a median 55 days on market. The difference between Redfin and NAR figures reflects methodology: NAR measures end-of-month unsold inventory via MLS, while Redfin tracks active listings in real time across its own feeds.

For deeper analysis, see US Housing Inventory: Current Supply and Months of Stock and Average Days on Market.

Mortgage Rates and Affordability

| Rate Type | Current Rate | Prior Week | Year Ago | 5-Year Avg |

|---|---|---|---|---|

| 30-Year Fixed | 6.51% | 6.36% | 6.86% | ~5.8% |

| 15-Year Fixed | 5.85% | 5.71% | 6.01% | ~5.1% |

Source: Freddie Mac Primary Mortgage Market Survey, week ending May 21, 2026

The 30-year fixed rate averaged 6.51% for the week ending May 21, 2026, according to Freddie Mac’s PMMS. Rates have stayed above 6% for four consecutive years.

The current level is 35 basis points below the year-ago rate of 6.86%, providing modest relief, but remains well above the sub-3% lows of 2021 that many current homeowners locked in.

Sam Khater, Freddie Mac’s Chief Economist, noted that “while purchase demand is softening, it remains above this time last year.”

Affordability Data

| Metric | Value | Period | YoY Change |

|---|---|---|---|

| NAR Housing Affordability Index | 110.6 | April 2026 | +9.2 pts |

| Median Household Income (est.) | ~$81,000 | 2025 ACS | +4.2% |

| Monthly Mortgage Payment (median home at 6.51%, 20% down) | ~$2,115 | May 2026 | -$85 vs May 2025 |

| Payment as % of Median Income | ~31.3% | May 2026 | -1.5 pts |

| Income Needed for Median Home | ~$110,000 | May 2026 | N/A |

Sources: NAR Housing Affordability Index; BLS; Freddie Mac. Mortgage payment calculated assuming median price $417,700, 20% down, 30-year fixed at 6.51%, excluding taxes and insurance.

The NAR Housing Affordability Index registered 110.6 in April 2026, up from 101.4 a year earlier, marking eight consecutive months of improvement. A reading above 100 means the median-income household can technically afford the median-priced home, though the margin remains thin.

At a 6.51% rate with 20% down on the median-priced home of $417,700, the monthly principal and interest payment is approximately $2,115. Adding property taxes and insurance pushes the effective monthly cost above $2,800 in most markets.

According to Realtor.com’s 2026 forecast, the typical mortgage payment as a share of median income is expected to dip to 29.3%, the first time it falls below 30% since 2022.

Every 1 percentage point increase in mortgage rates adds roughly $225 per month to the payment on a $417,700 home with 20% down.

The difference between today’s 6.51% and the 2.65% low of January 2021 represents approximately $850 per month in additional housing cost for the same home, a figure that quantifies the affordability shock of the rate environment.

For deeper affordability analysis, see Home Affordability in America and Mortgage Interest Rate History.

New Construction, Builder Sentiment, and Housing Starts

| Metric | Value | Period | MoM Change | YoY Change |

|---|---|---|---|---|

| Housing Starts (SAAR) | 1,465,000 | April 2026 | -2.8% | -2.1% |

| Single-Family Starts | 935,000 | April 2026 | -2.8% | N/A |

| Multi-Family Starts | 406,000 | April 2026 | +29.1% | N/A |

| Building Permits (SAAR) | 1,442,000 | April 2026 | +5.8% | -0.2% |

| New Home Sales (SAAR) | 682,000 | March 2026 | +7.4% | +3.3% |

| Median New Home Price | $387,400 | March 2026 | -5.3% | -6.2% |

| New Home Months of Supply | 8.5 | March 2026 | N/A | -7.6% |

Sources: US Census Bureau New Residential Construction, April 2026; US Census Bureau New Residential Sales, March 2026

Housing starts pulled back 2.8% month-over-month in April to 1.465 million SAAR, following a strong March that hit 1.502 million, the highest since December 2024. Single-family starts slipped to 935,000, while multi-family starts surged 29.1% to 406,000, reflecting renewed apartment construction activity.

New home sales rebounded 7.4% in March to 682,000 SAAR, partly recovering from January’s 587,000 reading, the weakest in over a year. But the median new home price tells the real story: at $387,400 in March 2026, it is now 6.2% below the year-ago level and $30,300 cheaper than the median existing home.

Builders are actively cutting prices and layering incentives to move elevated inventory. New home months of supply sits at 8.5, nearly double the existing-home market’s 4.4 months.

Builder Sentiment

| Month | HMI Score | Current Sales | Future Sales (6mo) | Buyer Traffic | Builders Cutting Prices |

|---|---|---|---|---|---|

| May 2026 | 37 | 40 | 45 | 25 | 32% |

| April 2026 | 34 | 37 | 42 | 22 | 36% |

| March 2026 | 38 | 42 | 49 | 25 | 37% |

| February 2026 | 37 | 41 | 47 | 24 | 36% |

| January 2026 | 37 | 40 | 44 | 24 | 30% |

Source: NAHB/Wells Fargo Housing Market Index, January through May 2026

The NAHB/Wells Fargo Housing Market Index rose to 37 in May 2026, up from April’s seven-month low of 34 but still firmly below the 50-point threshold that separates optimism from pessimism. May marked the 25th consecutive month below 50.

The price-cut data within the NAHB survey quantifies builder distress: 32% of builders cut prices in May with an average reduction of 6%, and 61% offered sales incentives, the 14th consecutive month above 60%. NAHB Chairman Bill Owens cited “higher mortgage rates, rising gas prices and economic uncertainty related to the war in Iran” as continuing demand dampeners.

NAHB Chief Economist Robert Dietz noted that “although some regional markets, including parts of the Midwest, are showing relative strength, the housing market continues to face significant affordability challenges.” Regional HMI scores in May ranged from 44 in the Northeast and 45 in the Midwest to 36 in the South and just 27 in the West.

Building permits, a leading indicator of future construction, came in at 1.442 million SAAR in April 2026. That is essentially flat year-over-year (-0.2%), suggesting builders are maintaining current activity levels rather than scaling up.

This points to a supply pipeline that will not meaningfully expand until either rates decline or buyer demand strengthens.

For detailed construction data, see New Home Construction Statistics and Housing Starts by State.

Housing Market Forecasts for 2026

| Forecaster | Price Change Forecast | Sales Volume Forecast | Rate Assumption | Date Issued |

|---|---|---|---|---|

| NAR (revised) | +4.0% | +4% existing sales | ~6.3% | March 2026 |

| Zillow | +1.2% | 4.26M existing (+4.3%) | Above 6% | December 2025 |

| Realtor.com | +2.2% | 4.13M existing (+1.7%) | ~6.3% | December 2025 |

| J.P. Morgan | 0% (flat) | N/A | N/A | January 2026 |

| S&P/Reuters Survey | +1.8% (Case-Shiller) | N/A | N/A | March 2026 |

| Fannie Mae | +3.0% (revised) | N/A | 6.3% (year-end) | Q1 2026 |

Sources: NAR March 2026 Forecast; Zillow 2026 Housing Forecast; Realtor.com 2026 Forecast; J.P. Morgan 2026 Outlook; Reuters survey; Fannie Mae ESR

Forecasts for the remainder of 2026 cluster around modest positive price growth but with an unusually wide range. Estimates span from J.P. Morgan’s flat 0% to NAR’s +4%, a 4-percentage-point spread that reflects genuine uncertainty about how tariffs, geopolitical risk, and rate movements will interact.

The consensus sits near +1.5% to 2.5% nationally. All forecasters assume mortgage rates will remain above 6% through year-end, limiting the potential for a volume breakout.

NAR revised its 2026 forecast downward in March, noting that “due to the upward trajectory of mortgage rates, NAR now expects existing-home sales to increase 4% this year, down from the previous projection.” New-home sales expectations were also revised to flat, from a prior forecast of 5% growth.

J.P. Morgan’s flat 0% forecast is the most bearish of the group. Their research team, led by Head of Securitized Products Research John Sim, pointed to a housing shortage they believe has been overestimated at 1.2 million homes, significantly below other industry estimates. They expect “home prices to stall at 0% nationally in 2026.”

A March 2026 Reuters survey of housing analysts projects the Case-Shiller Index to rise 1.8% in 2026 followed by 2.5% in 2027, reflecting a market “constrained on both sides: affordability pressures continue to limit demand, while insufficient resale supply prevents a deeper price correction.”

For individual forecaster analysis, see Housing Market Predictions and the Housing Market Forecast Comparison 2026.

For historical context on whether current conditions suggest crash risk, see Will the Housing Market Crash?

Year-Over-Year Comparison: 2024 vs 2025 vs 2026

| Metric | April 2024 | April 2025 | April 2026 | Trend |

|---|---|---|---|---|

| Existing Sales (SAAR) | 4.08M | 4.00M | 4.02M | Flat for 3 years |

| Median Price | $406,600 | $414,000 | $417,700 | Decelerating appreciation |

| Inventory | 1.21M | 1.39M | 1.47M | Gradually building |

| Months of Supply | 3.5 | 4.3 | 4.4 | Approaching balance |

| 30-Year Fixed Rate | 7.17% | 6.73% | 6.33% (Apr avg) | Declining slowly |

| Days on Market | 26 | 29 | 32 | Slowing pace |

| First-Time Buyers | 33% | 34% | 33% | Flat |

Sources: NAR Existing-Home Sales, April 2024-2026; Freddie Mac PMMS

The three-year comparison reveals the market’s structural pattern. Sales volume has oscillated within a 200,000-unit band for three consecutive Aprils. Prices have risen each year but at a decelerating pace: +5.7% in April 2024, +1.8% in April 2025, +0.9% in April 2026. Inventory has grown steadily from 1.21 million to 1.47 million over two years, adding roughly 130,000 units annually.

The most encouraging signal is in rates and affordability. The average April mortgage rate has fallen from 7.17% in 2024 to 6.33% in 2026, an 84-basis-point improvement that translates to roughly $190 per month in lower payments on the median-priced home.

Combined with income growth outpacing home prices, this has pushed the affordability index from below 100 (unaffordable for median household) to 110.6 (affordable with thin margin).

The most concerning signal is days on market, which has risen from 26 to 32 days over two years. Homes are selling more slowly, consistent with a market where buyer urgency has faded and inventory options have expanded.

This is a healthy normalization from the frantic 2021-2022 market, but it indicates that sellers can no longer expect immediate multiple-offer situations in most markets.

Byline: USPropertyStats Editorial Team Last Updated: May 2026 Next Update: August 2026 (Q2 data refresh)