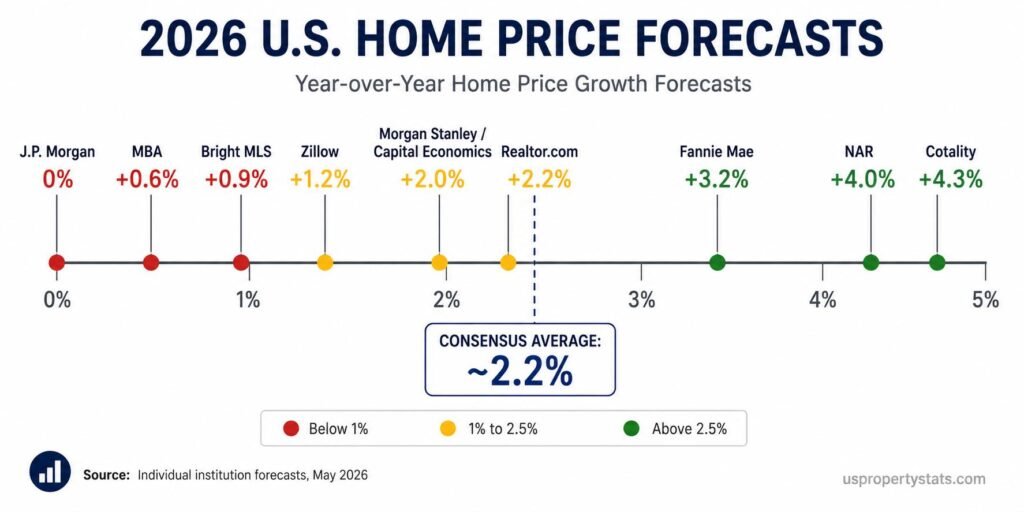

Major institutions forecast US home prices will rise between 0% and 4.3% in 2026, with the consensus of eight forecasters sitting at approximately 2.2%. NAR Chief Economist Lawrence Yun holds the most bullish position at +4.0%, while J.P. Morgan is the most bearish at flat 0%. Mortgage rates are expected to end 2026 between 5.8% and 6.4%, with no forecaster predicting a return below 6% before 2027.

This page compiles 2026 housing market predictions from eight major institutions covering home prices, sales volume, mortgage rates, and new construction. It also tracks what each forecaster predicted for 2024 and 2025 and how accurate those predictions turned out to be.

All forecasts are attributed to specific organizations with dates issued. Data current as of May 2026.

One critical context item before the data: the Iran War that began on February 28, 2026, materially disrupted forecasts issued at the start of the year.

US and Israeli strikes on Iran caused the 30-year mortgage rate to surge from a multi-year low of 5.98% in late February to 6.46% by early April, a 48-basis-point spike in five weeks. According to Inman, Fannie Mae had previously forecast 6.0% rates by year-end 2026.

That forecast did not survive the spring. The table below reflects each institution’s most recent updated forecast, not their January 2026 projections.

2026 Home Price Predictions: All Forecasters Compared

| Forecaster | 2026 Price Change | 2027 Price Change | Methodology | Date Updated |

|---|---|---|---|---|

| NAR | +4.0% | N/A | Median existing-home price YoY | April 2026 |

| Cotality (CoreLogic) | +4.3% | N/A | Case-Shiller, Oct 2025-Oct 2026 | Q1 2026 |

| Fannie Mae ESR | +3.2% | +1.9% | Home Price Index, Q4/Q4 | May 2026 |

| Realtor.com | +2.2% | N/A | Existing-home sale price YoY | December 2025 |

| Morgan Stanley | +2.0% | N/A | National home price index | Q1 2026 |

| Capital Economics | ~+2.0% | ~+2.0% | Case-Shiller Index | Q1 2026 |

| Zillow | +1.2% | N/A | Zillow Home Value Index (ZHVI) | Q1 2026 |

| Bright MLS | +0.9% | N/A | MLS transaction data | Q1 2026 |

| MBA | +0.6% | +0.5% | National home price index | December 2025 |

| J.P. Morgan | 0% (flat) | N/A | National price index | January 2026 |

The 4.3-percentage-point spread between the most bullish forecast (Cotality at +4.3%) and the most bearish (J.P. Morgan at 0%) is wider than typical for a single calendar year. This reflects genuine disagreement about three variables: whether the lock-in effect is loosening fast enough to release inventory, whether tariff-driven inflation will feed into housing costs, and whether the Iran War’s effect on mortgage rates is temporary or persistent.

NAR’s +4.0% forecast is driven by Lawrence Yun’s argument that “persistent supply shortages and demographic demand continue supporting valuations,” even as he has revised sales volume forecasts downward. J.P. Morgan’s flat 0% rests on their research team’s view that the US housing shortage has been significantly overestimated, with their analysts placing the true shortage at 1.2 million homes rather than the 3-4 million cited by other institutions.

The Fannie Mae Home Price Expectations Survey, which polls over 100 housing experts quarterly, projects median cumulative home price appreciation of approximately 14.8% through 2030, implying an average of roughly 2-3% annually. This long-range consensus sits between the bullish and bearish camps on 2026 specifically.

For current price data against which to judge these forecasts, see Median Home Price in the US and US Housing Market Statistics.

Mortgage Rate Forecasts for 2026 and 2027

| Forecaster | Q2 2026 (est.) | Q3 2026 (est.) | Q4 2026 | Q4 2027 |

|---|---|---|---|---|

| Fannie Mae ESR | 6.3% | 6.2% | 6.0% | 5.6% |

| MBA | 6.3% | 6.3% | 6.3-6.4% | 6.3% |

| NAR | 6.2% | 6.0% | 5.7-6.0% | N/A |

| Redfin | 6.3% | 6.3% | 6.3% | N/A |

| Consensus range | 6.1-6.4% | 6.0-6.3% | 5.8-6.4% | 5.6-6.3% |

The mortgage rate forecast consensus is unusually tight: all major institutions project the 30-year fixed rate to remain between 6.0% and 6.4% through the end of 2026. This represents a narrow corridor of change from the current 6.51%, and no forecaster expects rates below 6% before mid-2027 at the earliest. The MBA’s forecast is the most conservative, projecting 6.3-6.4% for all four quarters of 2026, essentially a flat year.

Fannie Mae’s May 2026 update is the most recent comprehensive forecast available, projecting rates ending 2026 at 6.0% before declining further to 5.6% by Q4 2027. However, this projection carries explicit caveats about the Iran War.

Inman’s analysis of the May forecast notes that Fannie Mae had previously forecast 6.0% rates by year-end before the February 28 strike, which caused rates to spike from 5.98% to 6.46% in roughly five weeks. The 2027 outlook for single-family starts was revised down from +2.7% to +0.4% in the same update.

The practical threshold most economists watch is 6.0%. At sub-6% rates, NAR estimates approximately 5.5 million additional households would qualify for the median-priced home, which would materially unlock both buyer demand and seller willingness to list. No forecaster currently expects the 6% threshold to be crossed before late 2026 or early 2027.

For historical context and the relationship between Fed policy and mortgage rates, see Mortgage Interest Rate History and Mortgage Rate Forecast 2026.

Home Sales Volume Predictions

| Forecaster | 2026 Existing Sales Forecast | YoY Change | 2026 New Sales Forecast | Date |

|---|---|---|---|---|

| Fannie Mae ESR | 4.46 million | +9.2% | N/A | May 2026 |

| Zillow | 4.26 million | +4.3% | N/A | Q1 2026 |

| Realtor.com | 4.13 million | +1.7% | N/A | December 2025 |

| NAR (revised) | ~4.16 million | +4.0% | Flat vs 2025 | March 2026 |

| MBA | N/A | N/A | N/A | N/A |

| 2026 pace (actual, April) | 4.02 million SAAR | Flat | 682,000 SAAR (March) | April 2026 |

Sales volume forecasts are running well ahead of actual 2026 performance so far. The April 2026 pace of 4.02 million SAAR is essentially flat year-over-year, while forecasters predicted gains of 1.7% to 9.2%. Fannie Mae’s 4.46 million forecast would require sales to average approximately 4.64 million SAAR for the remaining eight months of the year, a 15% acceleration from the current pace that would demand a significant and rapid shift in market conditions.

NAR revised its sales forecast downward in March 2026, cutting its original projection of 10-20% growth to approximately 4%, citing “lower consumer confidence and softer job growth” as continuing headwinds. Lisa Sturtevant, Chief Economist at Bright MLS, noted that “pent-up demand is there, but there’s a lot of unease about the direction of the job market and the broader economy, which may stifle the market in 2026.”

The new home sales market is tracking closer to forecasts. The March 2026 pace of 682,000 SAAR is up 3.3% year-over-year, consistent with modest growth projections. Builder price cuts and incentive programs are sustaining new home demand even as the resale market stagnates. For full sales data, see Home Sales Statistics: New and Existing Home Sales Data.

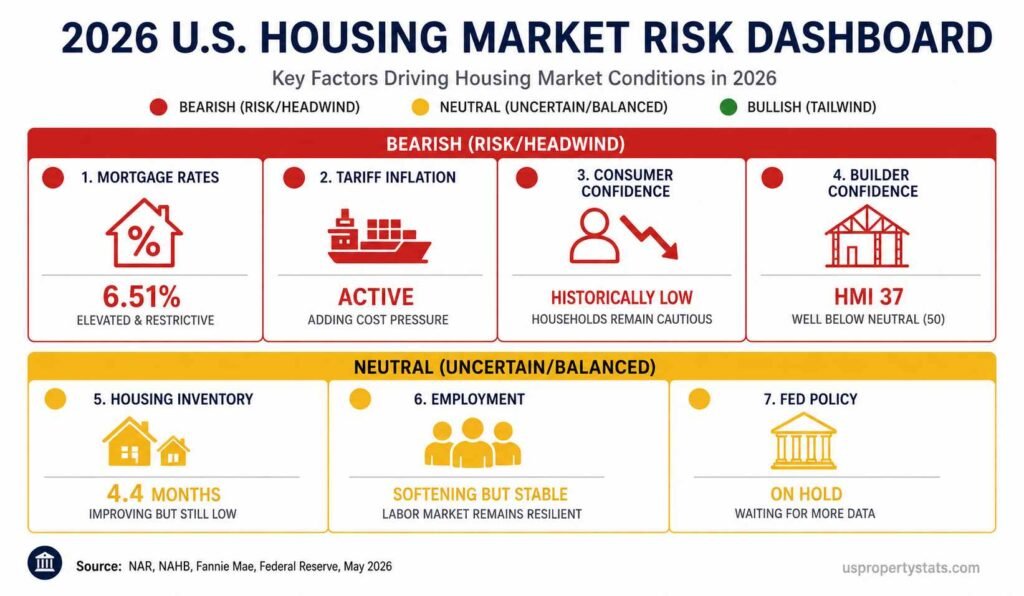

Key Risk Factors: Bull Case vs Bear Case

| Factor | Bull Case | Bear Case | Current Signal |

|---|---|---|---|

| Mortgage rates | Drop to 5.8% by Q4 2026 on Iran ceasefire + Fed cuts | Hold above 6.5% if Iran War escalates | Bearish (6.51%, trending up) |

| Inventory | YoY gains continue, approaching 5-month supply | Lock-in effect prevents meaningful unlock | Neutral (4.4 months, improving slowly) |

| Employment | Labor market holds, household formation continues | Job losses reduce qualifying buyers | Neutral (softening but stable) |

| Tariff inflation | Tariffs contained, construction cost impact limited | Materials costs spike, builder pullback accelerates | Bearish (tariffs active, NAHB HMI at 37) |

| Consumer confidence | Iran War resolution restores confidence | Prolonged uncertainty freezes discretionary purchases | Bearish (historically low per NAR data) |

| New construction | Builder incentives sustain new home sales above 700K | Starts decline further, worsening long-run supply | Neutral (starts pulling back, permits flat) |

| Fed policy | One or two rate cuts in H2 2026 | Fed holds rates, no cuts in 2026 | Neutral (Fed paused at Jan 2026 meeting) |

Of the seven risk factors, four currently read bearish or bearish-leaning. Mortgage rates are elevated and trending upward. Tariff inflation is active and feeding directly into construction costs. Consumer confidence is at historically low levels. Builder confidence has been below 50 for 25 consecutive months. The remaining three factors are neutral: inventory is improving but slowly, employment is softening but not collapsing, and Fed policy is on hold rather than tightening.

The single variable that could most rapidly shift the balance is the Iran War. Fannie Mae’s May 2026 analysis shows rates dropped to a multi-year low of 5.98% just before the February 28 strikes, demonstrating that the underlying rate trajectory was favorable before the geopolitical shock. A ceasefire or de-escalation that returns rates to the 6.0-6.1% range would unlock significant pent-up demand that has been building since 2022.

The scenario most forecasters consider unlikely but not impossible is J.P. Morgan’s flat 0% case. This would require rates to hold above 6.5% for the remainder of 2026 AND inventory to remain constrained enough that sellers can hold prices without capitulating.

Given that new home builders are already cutting prices 6% on average, a flat national number would require the existing-home market to offset continued new-home discounting. That is achievable given the resale market’s lock-in dynamics, but it would represent a historically unusual divergence between the two markets.

Forecast Accuracy: How Well Did Institutions Predict 2024 and 2025?

| Forecaster | 2024 Price Prediction | 2024 Actual | 2025 Price Prediction | 2025 Actual | Accuracy Rating |

|---|---|---|---|---|---|

| NAR | +2.5% | +4.5% (NAR) | +3.0% | +1.7% | Mixed |

| Fannie Mae ESR | +1.5% | +4.5% | +3.6% | +1.7% | Missed low both years |

| Zillow | -1.0% to flat | +4.5% | +2.0% | +1.7% | Missed badly in 2024 |

| Realtor.com | +1.7% | +4.5% | +1.0% | +1.7% | Missed low in 2024 |

| MBA | -2.0% | +4.5% | +1.0% | +1.7% | Missed badly in 2024 |

| J.P. Morgan | flat | +4.5% | +3.0% | +1.7% | Missed low in 2024 |

The 2024 forecasting record exposes a consistent bias across all major institutions: nearly every forecaster underestimated home price growth in 2024. The actual NAR year-over-year gain of approximately 4.5% exceeded every published forecast, several of which predicted outright price declines.

The MBA’s -2.0% prediction and Zillow’s -1.0% to flat range were the most severely wrong. The common error was overestimating how much the high-rate environment (30-year rates averaging above 7% for much of 2024) would suppress prices.

The 2025 actual outcome of approximately +1.7% was closer to forecasts but still fell below most predictions. NAR and Fannie Mae, the most bullish for 2025 at +3.0% and +3.6% respectively, overshot the actual. This reversal from 2024 suggests the forecasting models are still struggling to accurately weight the lock-in effect, which keeps prices elevated by suppressing supply regardless of demand conditions.

The practical takeaway from the accuracy table: institutional housing price forecasts have a documented bias toward being either too pessimistic or too optimistic by 2-3 percentage points, and the direction of the error often reverses year-over-year.

Use the consensus range (currently +1.2% to +4.0%) as a probability band rather than treating any single institution’s forecast as a reliable point prediction. For more on historical market cycles, see History of US Housing Market Crashes and US Housing Market Year-by-Year Since 2000.

Regional and Segment Predictions

| Region / Segment | Price Outlook | Key Driver | Forecaster |

|---|---|---|---|

| Northeast | +4% to +6% | Severe inventory shortage, NYC spillover demand | NAR Q1 2026 |

| Midwest | +3% to +5% | Relative affordability, migration inflows | NAR Q1 2026 |

| South | 0% to +2% | High new construction, insurance cost headwinds | NAR Q1 2026 |

| West | -2% to +1% | Post-pandemic correction, affordability exhaustion | NAR Q1 2026 |

| New construction nationally | -5% to -7% (prices) | Builder incentives, excess inventory, discounting | Census Bureau March 2026 |

| Entry-level homes (<$300K) | +3% to +5% | Acute shortage, first-time buyer demand | Zillow, NAR |

| Luxury homes (>$1M) | +1% to +3% | Stock market wealth effect, less rate-sensitive | Multiple |

The regional outlook confirms the two-speed market dynamic visible in current data. The Northeast and Midwest are tracking well above the national consensus, driven by inventory shortages so severe that demand has not meaningfully softened even at 6.5% rates.

NAR’s Q1 2026 data shows prices rose in 71% of 235 tracked metro areas, with 7% posting double-digit gains. The strongest gains are concentrated in New Jersey, Connecticut, Massachusetts, Illinois, Ohio, and Michigan.

The South and West face structural headwinds that the Northeast and Midwest do not. Florida’s combination of elevated insurance costs following 2024’s back-to-back hurricanes (Milton and Helene), a surge in new construction across Tampa Bay and Orlando, and affordability exhaustion in pandemic-era boomtowns has produced active price declines in multiple metros. Texas is similarly challenged by high new home inventory and softening in-migration from California, which had been a major demand driver in 2020-2022.

The entry-level segment below $300,000 is the tightest submarket in the country. Zillow Research notes that entry-level inventory has declined at a faster rate than mid-tier or luxury inventory as the lock-in effect disproportionately affects owners of lower-priced homes who have the largest rate differential between their existing mortgage and current market rates. This segment is likely to see the strongest appreciation regardless of what happens in the broader market. For detailed state-level data, see Home Appreciation Rates by State.

Byline: USPropertyStats Editorial Team | Last Updated: May 2026 | Next Update: August 2026